2022年12月鲍威尔今天凌晨的讲话实录

Today I will offer a progress report on the Federal Open Market Committee's (FOMC) efforts to restore price stability to the U.S. economy for the benefit of the American people. The report must begin by acknowledging the reality that inflation remains far too high. My colleagues and I are acutely aware that high inflation is imposing significant hardship, straining budgets and shrinking what paychecks will buy. This is especially painful for those least able to meet the higher costs of essentials like food, housing, and transportation. Price stability is the responsibility of the Federal Reserve and serves as the bedrock of our economy. Without price stability, the economy does not work for anyone. In particular, without price stability, we will not achieve a sustained period of strong labor market conditions that benefit all.

今天我想向诸位提供一份FOMC恢复美国经济价格稳定的进展报告,恢复价格稳定旨在造福美国人民。报告必须先承认通胀率仍然过高的现实。我和我的同事切身地意识到了高通胀正在造成重大的困难,使预算紧张而薪水的购买力也变得吃紧。对于那些最无力支付食品、住房和交通等必需品成本的人来说,通胀尤其痛苦。保持价格稳定是美联储的责任,也是我们经济的基石。没有价格稳定,经济对任何人都无济于事。需要强调的是,没有价格稳定,我们就无法实现惠及所有人的可持续的强劲劳动力市场状况。

We currently estimate that 12-month personal consumption expenditures (PCE) inflation through October ran at 6.0 percent (figure 1).1 While October inflation data received so far showed a welcome surprise to the downside, these are a single month's data, which followed upside surprises over the previous two months. As figure 1 makes clear, down months in the data have often been followed by renewed increases. It will take substantially more evidence to give comfort that inflation is actually declining. By any standard, inflation remains much too high.

根据我们目前的估计,截至今年10月的12个月个人消费支出(PCE)通胀率为6%(图1)。虽然迄今为止收到的10月份通胀数据显示出令人欣喜的下行意外,但这只是单月的数据,而此前我们才经历了两个月的通胀上行意外。正如图1所表明的,数据下降的当月往往紧随其后的是通胀的再度回升。我们需要更多的证据才能让我们确信通胀率确实在下降。从任何标准来看,通胀率仍然太高。

For purposes of this discussion, I will focus my comments on core PCE inflation, which omits the food and energy inflation components, which have been lower recently but are quite volatile. Our inflation goal is for total inflation, of course, as food and energy prices matter a great deal for household budgets. But core inflation often gives a more accurate indicator of where overall inflation is headed. Twelve-month core PCE inflation stands at 5.0 percent in our October estimate, approximately where it stood last December when policy tightening was in its early stages. Over 2022, core inflation rose a few tenths above 5 percent and fell a few tenths below, but it mainly moved sideways. So when will inflation come down?

在今天的讨论中,我将重点评论核心PCE通胀,即剔除了食品和能源的通胀,这两大部类最近走低但波动很大。当然,我们的通胀目标是总体通胀,因为食品和能源价格对家庭的预算有很大的影响。但是,核心通胀率往往能提供一个更准确的指明整体通胀走向的指标。在我们10月份的估计中,12个月的核心PCE通胀率为5%,大约是去年12月政策紧缩的早期阶段的水平。今年全年,核心通胀率在5%上下波动呈横向走势。那么问题来了,通胀率何时会回落?

I could answer this question by pointing to the inflation forecasts of private-sector forecasters or of FOMC participants, which broadly show a significant decline over the next year. But forecasts have been predicting just such a decline for more than a year, while inflation has moved stubbornly sideways. The truth is that the path ahead for inflation remains highly uncertain. For now, let's put aside the forecasts and look instead to the macroeconomic conditions we think we need to see to bring inflation down to 2 percent over time.

我们可以通过私人部门预测者或FOMC参与者的通胀预测来回答这个问题,预测广泛地指向了明年 (通胀)可能大幅下降。但是,一年多来,预测者一直在预测通胀会下降,而通胀却顽固地横向移动。事实是,通货膨胀的未来路径仍然非常不确定。现在,让我们抛开预测,审视我们认为需要看到的宏观经济条件,以便在一段时间内将通胀率降至2%。

For starters, we need to raise interest rates to a level that is sufficiently restrictive to return inflation to 2 percent. There is considerable uncertainty about what rate will be sufficient, although there is no doubt that we have made substantial progress, raising our target range for the federal funds rate by 3.75 percentage points since March. As our last postmeeting statement indicates, we anticipate that ongoing increases will be appropriate. It seems to me likely that the ultimate level of rates will need to be somewhat higher than thought at the time of the September meeting and Summary of Economic Projections. I will return to policy at the end of my comments, but for now, I will simply say that we have more ground to cover.

首先,我们需要将利率提高到一个有足够限制性的水平,使通胀恢复到2%。至于什么水平的利率才是足够限制性的则有很大的不确定性,尽管毫无疑问,我们已经取得了实质性的进展,自3月份以来,我们将联邦基金利率的目标区间范围提高了3.75%。正如联储上次的会后声明所指出的,我们预计持续提高利率将是适当的。在我看来,终端利率很可能需要比9月会议和经济预测摘要时的数字更高一些。我将在评论的最后回到政策问题上,但现在我只想说,我们还有更多的工作要做。

We are tightening the stance of policy in order to slow growth in aggregate demand. Slowing demand growth should allow supply to catch up with demand and restore the balance that will yield stable prices over time. Restoring that balance is likely to require a sustained period of below-trend growth.

我们正在收紧政策的立场,以遏制总需求的增长。需求增长放缓应当会使得供应赶上需求,恢复供需平衡,从而在一段时间内带来稳定的价格。恢复这种平衡可能需要一段持续的低于趋势水平的经济增长期。

Last year, the ongoing reopening of the economy boosted real gross domestic product (GDP) growth to a very strong 5.7 percent. This year, GDP was roughly flat through the first three quarters, and indicators point to modest growth this quarter, which seems likely to bring the year in with very modest growth overall. Several factors contributed to this slowing growth, including the waning effects of reopening and of pandemic fiscal support, the global implications of Russia's war against Ukraine, and our policy actions, which tightened financial conditions and are affecting economic activity, particularly in interest-sensitive sectors such as housing. We can say that demand growth has slowed, and we expect that this growth will need to remain at a slower pace for a sustained period.

去年,经济重启推升了美国的实际GDP增长,增速达到非常强劲的5.7%。今年,实际GDP在前三个季度基本持平,而各项指标显示本季度增长温和,这似乎可能使今年的总体经济增长非常温和。有几个因素致使增长放缓,包括重启和疫情期财政支持的消褪,俄乌冲突的全球影响,以及我们的货币政策行动,政策收紧了金融条件,正对经济活动构成影响,尤其是在房地产等对利率敏感的部门。经济需求的增长已经放缓,我们预计增长需要在一段持续期内保持较慢的速度。

Despite the tighter policy and slower growth over the past year, we have not seen clear progress on slowing inflation. To assess what it will take to get inflation down, it is useful to break core inflation into three component categories: core goods inflation, housing services inflation, and inflation in core services other than housing (figure 2).

尽管过去一年政策收紧且增长放缓,但我们仍未看到通胀放缓的明显进展。为了评估要怎样才能使通胀下降,需要将核心通胀率切分为三个组成部分进行分析:核心商品通胀率、住房服务通胀率和住房以外的核心服务通胀率(图2)。

Core goods inflation has moved down from very high levels over the course of 2022, while housing services inflation has risen rapidly. Inflation in core services ex housing has fluctuated but shown no clear trend. I will discuss each of these items in turn.

今年,核心商品通胀率已经从非常高的水平下降,而住房服务通胀率则迅速上升。除住房外的核心服务通胀率有所波动,但没有显露出明显的趋势。我将逐一探讨各个分项。

Early in the pandemic, goods prices began rising rapidly, as abnormally strong demand was met by pandemic-hampered supply. Reports from businesses and many indicators suggest that supply chain issues are now easing. Both fuel and nonfuel import prices have fallen in recent months, and indicators of prices paid by manufacturers have moved down. While 12-month core goods inflation remains elevated at 4.6 percent, it has fallen nearly 3 percentage points from earlier in the year. It is far too early to declare goods inflation vanquished, but if current trends continue, goods prices should begin to exert downward pressure on overall inflation in coming months.

在疫情的早期,商品价格开始迅速上涨,异常强劲的需求碰上了疫情导致的供应破坏。来自企业的报告和许多指标表明,供应链问题现在正在缓和。近几个月来,燃料和非燃料进口价格都有所下降,制造商支付的价格也有所下降。虽然12个月的核心商品通胀率仍然高达4.6%,但与今年年初相比已经下降了近3%。现在就宣称制服了商品通胀还为时尚早,但如果目前的趋势延续下去,商品价格应该在未来几个月开始对整体通胀产生下行压力。

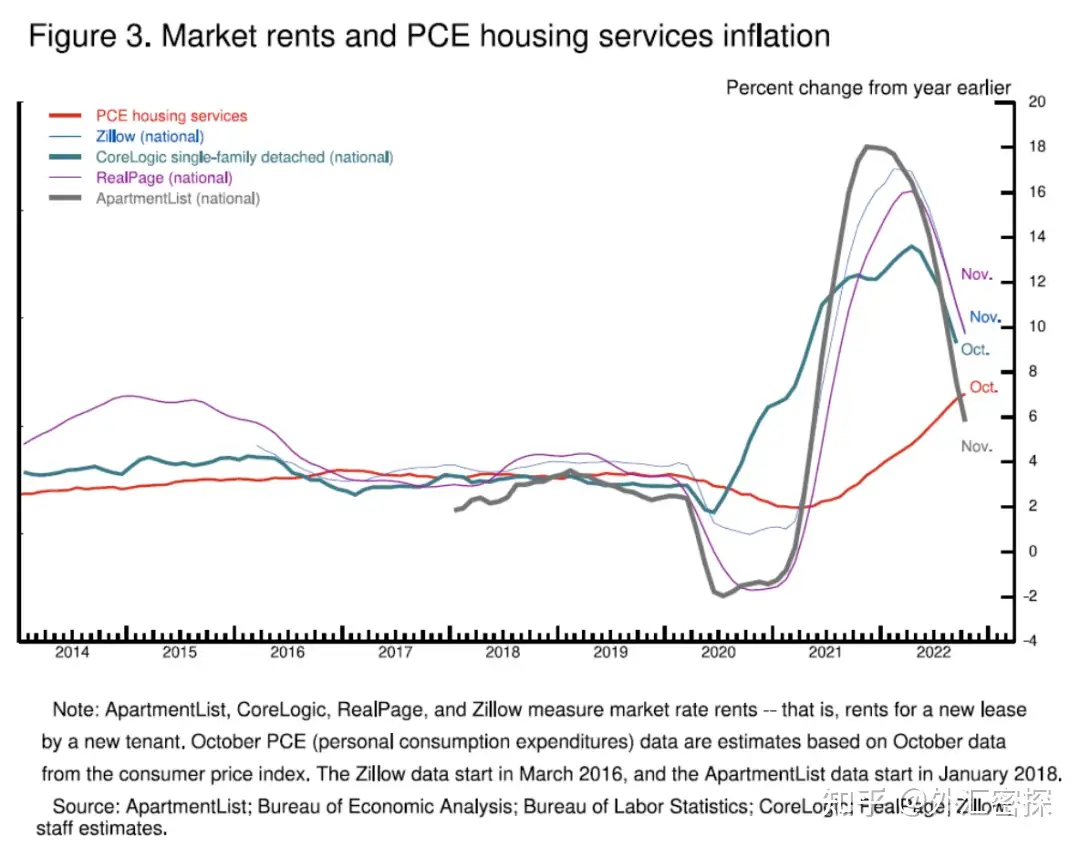

Housing services inflation measures the rise in the price of all rents and the rise in the rental-equivalent cost of owner-occupied housing. Unlike goods inflation, housing services inflation has continued to rise and now stands at 7.1 percent over the past 12 months. Housing inflation tends to lag other prices around inflation turning points, however, because of the slow rate at which the stock of rental leases turns over.2 The market rate on new leases is a timelier indicator of where overall housing inflation will go over the next year or so. Measures of 12-month inflation in new leases rose to nearly 20 percent during the pandemic but have been falling sharply since about midyear (figure 3).

住房服务通胀衡量的是所有租金价格的上涨和业主自住房的租金等值成本的上涨。与商品通胀不同,住房服务通胀持续上升,在过去12个月中为7.1%。然而,在通胀的转折点,住房通胀往往会滞后于其他价格,因为租约重置的速度较慢。在疫情期间,新租约的12个月通胀率上升到近20%,但自年中以来一直在急剧下降(图3)。

As figure 3 shows, however, overall housing services inflation has continued to rise as existing leases turn over and jump in price to catch up with the higher level of rents for new leases. This is likely to continue well into next year. But as long as new lease inflation keeps falling, we would expect housing services inflation to begin falling sometime next year. Indeed, a decline in this inflation underlies most forecasts of declining inflation.

如图3所示,随着现有租约的重置和价格跳升,以赶上新租约的更高租金水平,整体住房服务通胀持续上升。这种情况可能会持续到明年。但是,只要新租约的通货膨胀率持续下降,我们预计住房服务通货膨胀率将在明年某个时点开始下降。事实上,这部分通胀的下降是大多数通胀下降预测的基础。

Finally, we come to core services other than housing. This spending category covers a wide range of services from health care and education to haircuts and hospitality. This is the largest of our three categories, constituting more than half of the core PCE index. Thus, this may be the most important category for understanding the future evolution of core inflation. Because wages make up the largest cost in delivering these services, the labor market holds the key to understanding inflation in this category.

最后,我们来看看住房以外的核心服务。这一支出类别涵盖了从医疗保健和教育到理发和招待的广泛服务。这是我们三个类别中最大的一个分项,占核心PCE的一半以上。因此,这可能是理解核心通胀未来演变的最重要分项。由于工资构成了提供这些服务的最大成本,劳动力市场是理解这一类别通胀的关键。

In the labor market, demand for workers far exceeds the supply of available workers, and nominal wages have been growing at a pace well above what would be consistent with 2 percent inflation over time.3 Thus, another condition we are looking for is the restoration of balance between supply and demand in the labor market.

在劳动力市场上,对工人的需求远远超过了现有工人的供应,名义工资的增长速度远远超过了与2%的通胀率相一致的水平。因此,我们要寻找的另一个压低通胀的条件是恢复劳动力市场的供需平衡。

Signs of elevated labor market tightness emerged suddenly in mid-2021. The unemployment rate at the time was much higher than the 3.5 percent that had prevailed without major signs of tightness before the pandemic. Employment was still millions below its level on the eve of the pandemic. Looking back, we can see that a significant and persistent labor supply shortfall opened up during the pandemic—a shortfall that appears unlikely to fully close anytime soon.

劳动力市场紧凑的迹象在2021年中期突然浮现。当时的失业率远远高于疫情之前未有紧凑迹象的3.5%的水平。就业水平仍然比疫情前的水平低了数百万。回顾过去,我们可以看到,疫情期出现了重大且持续的劳动力供应短缺——而这种短缺似乎不太可能被很快解决。

Comparing the current labor force with the Congressional Budget Office's pre-pandemic forecast of labor force growth reveals a current labor force shortfall of roughly 3-1/2 million people (figure 4, left panel).4 This shortfall reflects both lower-than-expected population growth and a lower labor force participation rate (figure 4, right panel). Participation dropped sharply at the onset of the pandemic because of many factors, including sickness, caregiving, and fear of infection. Many forecasters expected that participation would move back up fairly quickly as the pandemic faded. And for workers in their prime working years, it mostly has. Overall participation, however, remains well below pre-pandemic trends.

将目前的劳动力水平与国会预算办公室对劳动力增长的预测相比较,我们可以看到目前的劳动力缺口大约为350万(图4,左图)。这一缺口既反映了人口增长低于预期,也反映了劳动参与率的下降(图4,右图)。由于许多因素,包括疾病、护理和对感染的恐惧,参与率在疫情开始时急剧下降。许多预测者预计,随着疫情的消退,参与率将迅速回升。对于正值黄金工作年龄段的工人来说,参与率确实回升了。然而,总体参与率仍然远远低于疫情前的趋势。

Some of the participation gap reflects workers who are still out of the labor force because they are sick with COVID-19 or continue to suffer lingering symptoms from previous COVID infections ("long COVID").5 But recent research by Fed economists finds that the participation gap is now mostly due to excess retirements—that is, retirements in excess of what would have been expected from population aging alone.6 These excess retirements might now account for more than 2 million of the 3‑1/2 million shortfall in the labor force.7

一部分的参与率缺口反映了那些因为患有新冠肺炎或遭受“长新冠”困扰而仍未加入劳动力大军的工人。但美联储经济学家最近的研究发现,参与率的缺口现在主要是由于超额退休——即退休人数超出了由人口老龄化所推算的水平。这部分超额退休人员现在可能占到劳动力320万缺口中的200万以上。

What explains these excess retirements? Health issues have surely played a role, as COVID has posed a particularly large threat to the lives and health of the elderly.8 In addition, many older workers lost their jobs in the early stages of the pandemic, when layoffs were historically high. The cost of finding new employment may have appeared particularly large for these workers, given pandemic-related disruptions to the work environment and health concerns.9 Also, gains in the stock market and rising house prices in the first two years of the pandemic contributed to an increase in wealth that likely facilitated early retirement for some people.

是什么原因导致了超额退休?健康问题肯定发挥了作用,因为新冠肺炎对老年人的生活和健康构成了极大的威胁。此外,许多老年工人在疫情的早期阶段失去了工作,当时的裁员率是历史上最高的。考虑到与疫情有关的工作环境的破坏和健康问题,对这些老年工人而言,寻找新工作的成本可能特别大。此外,在疫情的头两年,股票市场的收益和房价的上涨促进了财富的增加,可能有助于一些人提前退休。

The data so far do not suggest that excess retirements are likely to unwind because of retirees returning to the labor force. Older workers are still retiring at higher rates, and retirees do not appear to be returning to the labor force in sufficient numbers to meaningfully reduce the total number of excess retirees.10

迄今为止的数据并不能保证超额退休人员有可能因为退休人员重返劳动力市场而得到缓解。老年工人的退休率仍然较高,而退休人员返回劳动力的数量似乎不足以有意义地减少超额退休人员的总数。

The second factor contributing to the labor supply shortfall is slower growth in the working-age population. The combination of a plunge in net immigration and a surge in deaths during the pandemic probably accounts for about 1-1/2 million missing workers.11

导致劳动力供应短缺的第二个因素是工作年龄人口的增长放缓。净移民人数的骤减和疫情期间死亡人数的激增可能是造成约150万工人“消失”的原因。

Policies to support labor supply are not the domain of the Fed: Our tools work principally on demand. Without advocating any particular policy, however, I will say that policies to support labor force participation could, over time, bring benefits to the workers who join the labor force and support overall economic growth. Such policies would take time to implement and have their effects, however. For the near term, a moderation of labor demand growth will be required to restore balance to the labor market.

支持劳动力供应的政策不在美联储的管辖范围内。我们的工具主要是在需求方面发挥作用。然而,在不提倡任何特定政策的情况下,我要说的是,随着时间的推移,支持劳动参与率的政策可以为加入劳动力的工人带来好处,并支持整体经济增长。可这种政策需要时间来实施并产生效果。就短期来说,我们亟需缓和劳动力需求的增长来恢复劳动力市场的平衡。

Currently, the unemployment rate is at 3.7 percent, near 50-year lows, and job openings exceed available workers by about 4 million—that is about 1.7 job openings for every person looking for work (figure 5). So far, we have seen only tentative signs of moderation of labor demand. With slower GDP growth this year, job gains have stepped down from more than 450,000 per month over the first seven months of the year to about 290,000 per month over the past three months. But this job growth remains far in excess of the pace needed to accommodate population growth over time—about 100,000 per month by many estimates. Job openings have fallen by about 1.5 million this year but remain higher than at any time before the pandemic.

目前的失业率为3.7%,接近50年来的最低点,职位空缺则超过现有工人约400万,即每一个找工作的人对应大约1.7个职位空缺(图5)。迄今为止,我们只看到劳动力需求缓和的初步迹象。随着今年GDP增长的放缓,就业岗位的增加已经从今年前七个月的每月45万个以上降至过去三个月的每月29万个左右。但这一就业增长仍然远远超过了适应人口增长所需的速度,即许多人所估算的每月约10万个。今年职位空缺已经减少了约150万个,但仍然高于疫情前的任何时候。

Wage growth, too, shows only tentative signs of returning to balance. Some measures of wage growth have ticked down recently (figure 6). But the declines are very modest so far relative to earlier increases and still leave wage growth well above levels consistent with 2 percent inflation over time. To be clear, strong wage growth is a good thing. But for wage growth to be sustainable, it needs to be consistent with 2 percent inflation.

工资增长也仅仅显示出重归平衡的初步迹象。一些衡量工资增长的指标最近有所下降(图6)。但是,相对于早先的工资增长,迄今为止的下降是非常温和的,并且仍然使工资增长远远高于与2%的通胀率相一致的水平。明确地说,强劲的工资增长是一件好事。但是,为了使工资增长能够持续,它需要与2%的通胀率相一致。

Let's sum up this review of economic conditions that we think we need to see to bring inflation down to 2 percent. Growth in economic activity has slowed to well below its longer-run trend, and this needs to be sustained. Bottlenecks in goods production are easing and goods price inflation appears to be easing as well, and this, too, must continue. Housing services inflation will probably keep rising well into next year, but if inflation on new leases continues to fall, we will likely see housing services inflation begin to fall later next year. Finally, the labor market, which is especially important for inflation in core services ex housing, shows only tentative signs of rebalancing, and wage growth remains well above levels that would be consistent with 2 percent inflation over time. Despite some promising developments, we have a long way to go in restoring price stability.

让我们来总结一下今天我对经济状况的回顾——即我们认为要将通胀率降至2%所需要看到的经济状况。经济活动的增长已经放缓,远远低于其长期趋势,这需要保持。商品生产的瓶颈正在缓解,商品价格通胀似乎也在缓解,这也必须维持下去。住房服务通胀可能会一直上升到明年,但如果新租约的通胀继续下降,我们将可能看到住房服务通胀在明年晚些时候开始下降。最后,对于除住房外的核心服务通胀尤为重要的劳动力市场,只显示出再平衡的初步迹象,工资增长仍然远远高于与2%的通胀率长期保持一致的水平。尽管有一些好转的迹象,可我们在恢复价格稳定方面还有很长的路要走。

Returning to monetary policy, my FOMC colleagues and I are strongly committed to restoring price stability. After our November meeting, we noted that we anticipated that ongoing rate increases will be appropriate in order to attain a policy stance that is sufficiently restrictive to move inflation down to 2 percent over time.

回到货币政策,我和FOMC的同事们坚定地致力于恢复价格稳定。在我们11月的会议后,我们指出,我们预计持续的加息将是适当的,以达到一个足以限制通胀率在一段时间内下降到2%的政策姿态。

Monetary policy affects the economy and inflation with uncertain lags, and the full effects of our rapid tightening so far are yet to be felt. Thus, it makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down. The time for moderating the pace of rate increases may come as soon as the December meeting. Given our progress in tightening policy, the timing of that moderation is far less significant than the questions of how much further we will need to raise rates to control inflation, and the length of time it will be necessary to hold policy at a restrictive level. It is likely that restoring price stability will require holding policy at a restrictive level for some time. History cautions strongly against prematurely loosening policy. We will stay the course until the job is done.

货币政策对经济和通货膨胀的影响具有不确定的滞后性,而且我们迄今为止的快速紧缩政策的全部效果还没有显现出来。因此,当我们接近足以使通货膨胀率下降的约束水平时,放缓我们的加息步伐是说得通的。放缓加息步伐的时机可能最快在12月的议息会议上到来。考虑到我们在政策紧缩方面的进展,放缓的时间节点远没有我们需要进一步提高利率以控制通货膨胀,且有必要将政策保持在限制性水平的持续期等问题重要。恢复价格稳定可能需要在一段时间内将政策保持在限制性水平。历史警示我们不要过早地放松政策。我们将坚持到底,直到大功告成。